Monday, January 31, 2005

Stockcoach the bagholder

What a lousy day! Well, here’s my sorry tale: I had a limit order to buy 2000 shares of COLL at $5.75 per share. Bargain price I thought for a profitable company with over $200 million in sales and a market cap of about $30 million. I had the limit order in place for about 2 weeks, hoping someone would bail out, allowing me to pick up some shares on the cheap. Oh, I got my shares all right. You see, at about 2:00 pm the company announced that it was delaying its annual report and may restate its earnings. Well, you can imagine what happened.

Would you like paper or plastic Mr. Stockcoach?

Neither thanks. Within minutes, my limit order was filled at $5.75. Needless to say, the stock got hammered. It finished the day at $4.85 (and down more in after-hours). And now I’m looking at a $2000 paper loss. Who do I blame? Well, I suppose I was partly at fault for having the limit order just sitting there in the first place. And it was certainly my fault for placing such a large order (last time I do that, lesson learned!). But realistically, trying to buy small cap stocks without a limit order is even more stupid. Anyway, what the heck was the company doing announcing this at 2:00 in the afternoon??? Stuff like that should be announced when the market is closed. I blame myself to some extent, but I blame the company even more.

What to do now? Not sure. The news actually wasn’t that bad. Yeah, I know restatements can be ugly. But I have seen my fair share of restatements, and I suspect this one won’t be that bad (if it happens at all). Under $5, this company is a good hold for the long term. And I suspect I may end up holding it for sometime cause I’m not prepared to realize my loss just yet. Heck, if it goes to $4 I may buy some more (though probably not considering how peeved I am at the company right now).

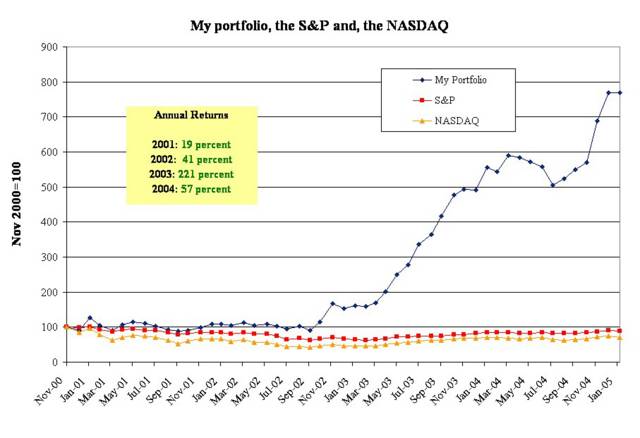

Anyhow, I’m glad January is over. I ended the month down 0.2 percent, compared to the S&P and Nasdaq, which dropped 2.5 percent and 5.2 percent, respectively. Though I still outperformed the major indices, the margin of outperformance slipped considerably over the past 5 trading days. I’ve updated the charts on the right, and included a little table in the first chart showing the percentage gain in my portfolio in each year starting from 2001.

Let’s hope February is a more profitable month than January!

Would you like paper or plastic Mr. Stockcoach?

Neither thanks. Within minutes, my limit order was filled at $5.75. Needless to say, the stock got hammered. It finished the day at $4.85 (and down more in after-hours). And now I’m looking at a $2000 paper loss. Who do I blame? Well, I suppose I was partly at fault for having the limit order just sitting there in the first place. And it was certainly my fault for placing such a large order (last time I do that, lesson learned!). But realistically, trying to buy small cap stocks without a limit order is even more stupid. Anyway, what the heck was the company doing announcing this at 2:00 in the afternoon??? Stuff like that should be announced when the market is closed. I blame myself to some extent, but I blame the company even more.

What to do now? Not sure. The news actually wasn’t that bad. Yeah, I know restatements can be ugly. But I have seen my fair share of restatements, and I suspect this one won’t be that bad (if it happens at all). Under $5, this company is a good hold for the long term. And I suspect I may end up holding it for sometime cause I’m not prepared to realize my loss just yet. Heck, if it goes to $4 I may buy some more (though probably not considering how peeved I am at the company right now).

Anyhow, I’m glad January is over. I ended the month down 0.2 percent, compared to the S&P and Nasdaq, which dropped 2.5 percent and 5.2 percent, respectively. Though I still outperformed the major indices, the margin of outperformance slipped considerably over the past 5 trading days. I’ve updated the charts on the right, and included a little table in the first chart showing the percentage gain in my portfolio in each year starting from 2001.

{kind=link}

Let’s hope February is a more profitable month than January!

Friday, January 28, 2005

Weekly Summary

I managed to stay in the black today, but my portfolio was still down $2,188 for the week, falling to $374,662. Since last Friday, I have underperformed the major indices by about 1 percent. It appears that attention has shifted a bit towards large cap stocks. Almost all the small cap and microcap stocks that I follow either went nowhere or drifted down this week. Hopefully next week will bring more favorable results.

Even more about Cramer’s investment performance!

Okay, perhaps I jumped the gun by giving Cramer credit for handily beating the S&P 500 over the past 3 years. The facts are not in question: Cramer’s Realmoney portfolio did beat the S&P by about 6 percent annually since the beginning of January 2002.

What’s at issue is the interpretation of this result. Let me explain. Cramer invests in relatively large stocks that comprise the S&P 500. Thus, it seems reasonable that one should compare his results to the S&P 500. Yes, but not quite. You see, when investors pick stocks from the S&P 500, they don’t typically weight their portfolios by the capitalization of each stock. So if I wanted to buy Intel and Tupperware because I thought they were both great companies, there’s no reason why I would buy 100 times more TUP than INTC simply because INTC has a market capitalization 100 times that of TUP.

Thus, when benchmarking performance, one should use an index that gives equal weight to the stocks in the S&P 500 (the equal weight index), as opposed to the standard S&P 500 index that one always sees that weights the stocks based on their market capitalization. Now, as it turns out, over long periods of time, the market capitalization S&P 500 index tends to yield about the same return as the equal weighted S&P 500 (well, almost as large since midcaps have historically outperformed large caps by a small margin). However, as this chart shows (after opening, click the 'compare to' button), the past 5 years have been exceptional, with the equal weight index outpacing the market cap index by an incredible 55 percent on a cumulative basis. Since the beginning of 2002 (when Cramer's portfolio was formed), the equal weighted S&P 500 index has outperformed the market cap weighted S&P 500 index cumulatively by about 22 percent. Moreover, the equal weighted S&P 500 index has even outperformed the Russell 2000 over that time.

And by how much has Cramer outperformed the market cap weighted S&P 500 in that time? Oh, by about 22 percent. In other words, Cramer’s portfolio has done no better than the equal weight S&P 500 index. Now, I am not going to disparage the Street.com for advertising the fact that Cramer has beaten the market cap weighted S&P 500. That’s the benchmark that everyone uses, including myself. Furthermore, no matter whether one likes or dislikes him, it's hard to deny that he is a smart guy with lots of brilliant insight into how the stock market works. However, the fact remains that Cramer’s portfolio has done about as well over the past 3 years as the average return on 1 million portfolios constructed by taking the stock picks of 1 million monkeys throwing darts at a list of stocks in the S&P 500. Come to think of it, there is a certain simian quality about the guy...

What’s at issue is the interpretation of this result. Let me explain. Cramer invests in relatively large stocks that comprise the S&P 500. Thus, it seems reasonable that one should compare his results to the S&P 500. Yes, but not quite. You see, when investors pick stocks from the S&P 500, they don’t typically weight their portfolios by the capitalization of each stock. So if I wanted to buy Intel and Tupperware because I thought they were both great companies, there’s no reason why I would buy 100 times more TUP than INTC simply because INTC has a market capitalization 100 times that of TUP.

Thus, when benchmarking performance, one should use an index that gives equal weight to the stocks in the S&P 500 (the equal weight index), as opposed to the standard S&P 500 index that one always sees that weights the stocks based on their market capitalization. Now, as it turns out, over long periods of time, the market capitalization S&P 500 index tends to yield about the same return as the equal weighted S&P 500 (well, almost as large since midcaps have historically outperformed large caps by a small margin). However, as this chart shows (after opening, click the 'compare to' button), the past 5 years have been exceptional, with the equal weight index outpacing the market cap index by an incredible 55 percent on a cumulative basis. Since the beginning of 2002 (when Cramer's portfolio was formed), the equal weighted S&P 500 index has outperformed the market cap weighted S&P 500 index cumulatively by about 22 percent. Moreover, the equal weighted S&P 500 index has even outperformed the Russell 2000 over that time.

And by how much has Cramer outperformed the market cap weighted S&P 500 in that time? Oh, by about 22 percent. In other words, Cramer’s portfolio has done no better than the equal weight S&P 500 index. Now, I am not going to disparage the Street.com for advertising the fact that Cramer has beaten the market cap weighted S&P 500. That’s the benchmark that everyone uses, including myself. Furthermore, no matter whether one likes or dislikes him, it's hard to deny that he is a smart guy with lots of brilliant insight into how the stock market works. However, the fact remains that Cramer’s portfolio has done about as well over the past 3 years as the average return on 1 million portfolios constructed by taking the stock picks of 1 million monkeys throwing darts at a list of stocks in the S&P 500. Come to think of it, there is a certain simian quality about the guy...

{kind=link}

Thursday, January 27, 2005

James Cramer's Investment Porfolio -- Follow up

Scott, who has a free subscription to Realmoney, delivers the goods: Cramer has averaged 9.3 percent annual return since Jan 1, 2002 versus 2.3 percent on the S&P 500. Mind you, smaller companies have outperformed the S&P over the past 3 years, and so Cramer's performance wouldn't look as great if we were to compare it to the Russel 2000. Still, anyway you cut, he has outperformed the market (and even the Russel 2000), and should get credit for that.

Lost another one to Nasdaq!

Third day in a row now that the Ponzidaq has outperformed Stockcoach. What's up with that? Yeah, I know, three days hardly makes a trend, but still... Well, at least I can take some comfort that TZOO fell today and that GIGM, one of my recent purchases, went up. Still, the gains in those two stocks weren't enough to offset the losses in the rest of my portfolio. The bottom line is that my portfolio fell by $1,100 today. Unless tomorrow turns out to be a great day, it looks like I'll be down for the week.

Wednesday, January 26, 2005

Jim Cramer's investment portfolio

So I was watching Screechy and Preachy and started thinking to myself: just how good is Cramer? The Street.com charges subscribers $320 a year to hear what stocks he is buying and selling in this personal portfolio, but where is the public record of how well his portfolio has performed? If anyone knows, please leave a comment.

How come I wasn't invited to the party?

Well yippee for the Nasdaq. Once again, the Nasdaq was up nicely today. Stockcoach, on the other hand, only managed to weasel out a measly $400 gain thanks to a good move by ASIA. If it hadn't been for ASIA, I would have been in the red again. Well, I suppose I shouldn't complain too much. I purposely rejigged my portfolio back in September so that it would have a beta as close to zero as possible. Thus, I shouldn't lament when I underperform the market when the market goes up (and similarly, I shouldn't take credit for the fact that my portfolio outperforms the market when the market goes down).

Tuesday, January 25, 2005

I hate Travelzoo

I should have known better than to equate Travelzoo with the Planet of the Apes in yesterday's post. You see, in the sequel to the Planet of the Apes, the apes rise again. And that's just what happened today. Stupid stupid TZOO went up 10 percent.

Travelzoo is the stock market's equivalent of William Hung: anyone with any sense knows he can't sing, yet there he is, absorbing the limelight, well past his 15 minutes of fame. Ahh... perhaps I'm being too harsh. I did, after all, present a theoretical example in an earlier post of why it may be profitable for investors to buy a stock even when everyone agrees that the stock is overvalued. Still, I hardly suspect that too many people are buying TZOO because of some sophisticated trading argument. These sad folk are bagholders plain and simple, and sooner or later they will pay the price for their ignorance. As far as I'm concerned, hopefully sooner rather than later.

Anway, due to TZOO and dips in GTSI and MRM (two of my largest holdings), my portfolio was down $460 today.

Travelzoo is the stock market's equivalent of William Hung: anyone with any sense knows he can't sing, yet there he is, absorbing the limelight, well past his 15 minutes of fame. Ahh... perhaps I'm being too harsh. I did, after all, present a theoretical example in an earlier post of why it may be profitable for investors to buy a stock even when everyone agrees that the stock is overvalued. Still, I hardly suspect that too many people are buying TZOO because of some sophisticated trading argument. These sad folk are bagholders plain and simple, and sooner or later they will pay the price for their ignorance. As far as I'm concerned, hopefully sooner rather than later.

Anway, due to TZOO and dips in GTSI and MRM (two of my largest holdings), my portfolio was down $460 today.

Monday, January 24, 2005

Stick a banana in it. Travelzoo is dead!

Sanity has finally begun to return to the Planet of the Apes. Travelzoo plummeted 25 percent today. Nevertheless, TZOO remains a $20 stock with a $55 price tag. Though the stock may rebound a bit, I firmly believe that the bubble has burst: TZOO will NEVER see the highs it reached late last year again. The only question now is when to cover my short. Right now, I have a limit order in for $43 dollars. Depending on how the stock performs over the next few days, I may lower it.

Anyway, despite a nice gain on TZOO, my portfolio was down $1,200 today, representing a drop of about one third of one percent, about in line with the decline in the S&P 500 (though still much better than the hapless Ponizdaq).

Anyway, despite a nice gain on TZOO, my portfolio was down $1,200 today, representing a drop of about one third of one percent, about in line with the decline in the S&P 500 (though still much better than the hapless Ponizdaq).

Friday, January 21, 2005

Weekly Summary

All in all a good week. As of the close of trading today, my portfolio was worth $376,850, up $6,218 from last Friday. Today turned out to be a busy trading day, a rarity for me because I try to avoid excessive trading to the extent possible. Four trades in total:

- Sold my shares of EDAP. I had purchased them more than 2 years ago at $1.50 when they were trading below cash value. The company has executed reasonably well since then, but I think the stock has gotten ahead of itself. I bailed today and sold out $4.75.

- Bought back my shares (and then some) in BOSC. As faithful readers may recall, I sold them only a few weeks ago. However, that was in the midst of a major surge in the stock price as daytraders piled in with the hope of making a quick buck . Since then, the shares have fallen by 50 percent. At $2.40, the stock is now trading not far above cash value, and with growing revenues and its position in the hot VOIP sector, I think there is plenty of upside here, and relatively little downside.

- Bought shares in AVGN. This biotech is losing money but is trading well below cash value, which I think will give me lots of downside protection. The company is working on a cure for Parkinson’s disease. I don’t know whether they will succeed, but I’m willing to roll the dice on this one.

- Bought shares in GIGM. This is my third time in this stock, although this is first time that I’ve bought above $1. However, the company’s fundamentals and prospects have improved a lot over the past 6 months. Yet, it’s trading at close to cash value. At the very least, I think it should be a $2 stock.

Thursday, January 20, 2005

Are dividends a good thing?

David, over at Seeking Alpha, argues that dividend paying stocks are a mistake. He's essentially expressing an implication of the Modigliani Miller theorem: if the market rate of return equals the rate of return on reinvested capital, then it does not matter what the dividend payout ratio is. Of course, as he points out, buybacks are a more tax efficient way for firms to return cash to shareholders. Moreover, Glenn Hubbard and others have long argued that most firms can generate a much higher rate of return on reinvested capital than the market rate but can not do so due to asymmetric information in credit markets. This suggests that dividends may not only be bad for shareholders, but they may be bad for economic growth as well.

On the other hand, dividends can be a form of signaling by which honest firms can signal to the market that they care about shareholders by returning money to them today instead of taking the money and using it to purchase $6000 shower curtains (i.e. a bit like going to university to prove that you are bright, not because university makes you more productive). I think this helps explain the current fad for dividend paying stocks (especially in light of Enron and WorldCom).

On the other hand, dividends can be a form of signaling by which honest firms can signal to the market that they care about shareholders by returning money to them today instead of taking the money and using it to purchase $6000 shower curtains (i.e. a bit like going to university to prove that you are bright, not because university makes you more productive). I think this helps explain the current fad for dividend paying stocks (especially in light of Enron and WorldCom).

The Ponzidaq keeps crumbling

Another bad day for the NASDAQ. No surprise. I continue to think that stocks are overvalued, and tech stocks with their high P/E multiples, unpredictable earning and revenues, and dubious accounting standards (options expensing anyone?), continue to be the most overvalued of all. I just regret that I did not short more of them when the NASDAQ was hitting fresh 52 week highs in December. Alas, my experience with GOOG (I lost $4000 shorting it last year), caused me to be too cautious and so I ended up staying on the sidelines. However, I am still actively looking for new short candidates since I believe that U.S. equity markets still have farther to fall. Anyway, as far as today is concerned, despite nice gains on my short positions (especially Bubbleboy Travelzoo), my portfolio was down $600.

Wednesday, January 19, 2005

Stock screener

A reader asks what stockscreener I use. I do use the Yahoo Finance stock screener on occasion, largely because I am comfortable with Yahoo Finance. However, my preference is to use the free advanced stock screener on MSN Money. It's extremely powerful, and has good coverage of microcap stocks. It requires a download, but afterwards, it's quick and easy to use. And amazingly enough, Microsoft doesn't come out as the top pick in every screen that you run.

Back on top

I was able to buck the market's downdraft today. Up $4,500. The market continues to behave badly. The NASDAQ was down 1.5 percent today. And with EBAY's and QCOM's bad news after the close, tomorrow could be another downer. It's times like this that I am thankful that most of my stocks are microcaps, which seem to sing to their own tune, regardless of which way the market is going.

Tuesday, January 18, 2005

Yawn

My portfolio has gone into a state of hibernation. It managed to eke out a $1,200 gain today thanks to decent moves by ASIA and GTSI, but that's less than I would have made if my money had been in a broad index like SPY or QQQQ.

In other news, I sold my shares in ZCOM at the open (at $2.30 per share) after the company announced quarterly numbers that were worse than I expected. I don't typically dump a stock just because of one bad quarter, but the problems here seem more entrenched and I suspect it will be some time before they regain profitability. For the time being, I'd rather be on the sidelines.

I also added a new stock to my team: Goldfield. Don't let the name fool you: They are not engaged in gold production. It's a nice value stock with a market cap of $15 million and $30 million in annual sales, trading at 75 percent of book value, and generated cash from operations of $4 million last year. Good enough for me; I picked up 15,000 shares this morning at 57 cents per share.

In other news, I sold my shares in ZCOM at the open (at $2.30 per share) after the company announced quarterly numbers that were worse than I expected. I don't typically dump a stock just because of one bad quarter, but the problems here seem more entrenched and I suspect it will be some time before they regain profitability. For the time being, I'd rather be on the sidelines.

I also added a new stock to my team: Goldfield. Don't let the name fool you: They are not engaged in gold production. It's a nice value stock with a market cap of $15 million and $30 million in annual sales, trading at 75 percent of book value, and generated cash from operations of $4 million last year. Good enough for me; I picked up 15,000 shares this morning at 57 cents per share.

Friday, January 14, 2005

Weekly summary

My 5 week winning streak is over. Though I was up somewhat today, I finished the week down $3,916. My portfolio is now worth $370,632. Especially disheartening is that the NASDAQ and S&P were flat this week, while the Russel 2000 was up by almost 1 percent. Thus, I lost money in absolute terms and relative to the market. Well, I remain optimistic that next week will bring better results!

Thursday, January 13, 2005

Another bad day

From the frying pan and into the fire: down $3,700 today, making this the third day in a row that my portfolio has dropped in value. I take some comfort in the fact that the stock market also sold off by about 1 percent. However, my aim is to exceed the market's performance, not equal it, especially since I've made it clear before that I expect the stock market to perform poorly over the coming months and years. Hopefully, tomorrow will be a better day.

Wednesday, January 12, 2005

NASDAQ up, Stockcoach down

Down $2,400 today. No major losses; just no offsetting gains. Also, I lost money as renewed buying interest pulled up the shares of TZOO and America's favorite jailbird.

Tuesday, January 11, 2005

Momentum stocks hit a brick wall

The day began with Taser's plunge. Then other momentum stocks began to flounder. By the close of trading, the biggest decline list for the NASDAQ was a who's who of momentum stocks that finally fell back to earth. Hey, even stocks that soared last year simply because they rhymed with "Taser" cratered. About time I say. Fortunately, good ol' Travelzoo was on the list, down 13 percent. Still, if you ask me, Travelzoo's valuation still makes Taser look like Berkshire Hathaway. Anyway, despite nice gains on my short positions, my portfolio was still down $600 today.

I also added a new member to my portfolio: AVCS. It's another interesting smallcap stock; trading below book value; lots of terrific assets on the balance sheet; and lots of insider buying at prices much higher than what I paid. I suspect the only reason it went down is because a major holder of the stock was forced into liquidation, and was forced to dump nearly a million shares on the open market. Much of the selling appears to be over as volume has dried up, so I'm hoping we go higher from here. Still, the stock is not without risk, so please read the disclosure before you even consider following my lead.

I also added a new member to my portfolio: AVCS. It's another interesting smallcap stock; trading below book value; lots of terrific assets on the balance sheet; and lots of insider buying at prices much higher than what I paid. I suspect the only reason it went down is because a major holder of the stock was forced into liquidation, and was forced to dump nearly a million shares on the open market. Much of the selling appears to be over as volume has dried up, so I'm hoping we go higher from here. Still, the stock is not without risk, so please read the disclosure before you even consider following my lead.

Monday, January 10, 2005

Couldn't resist ... loaded up on ASIA

I couldn't resist loading up on ASIA today. I bought 4500 shares at about $4.60 per share. The stock has been gratuitously hit by what happened to UTSI. UTSI bounced back today, and I suspect ASIA will bounce back tomorrow.

TZOO, why won't you die?

Up $2000 today, no thanks to TZOO. Like a monster in a cheesy Hollywood horror movie, just when you think it's dead, Travelzoo rises up. What's sustaining this sack of dung at $95? Clearly, it's not valuation. Even notoriously optimistic Wall Street analysts are all giving it a big fat sell rating. No wonder, given the ridiculous valuation of TZOO's customer base. The only thing sustaining the current price it is the expectation of another short squeeze, made possible by moronic new regulations passed by the SEC to curb naked shorting. Well, I have news for TZOO longs: sooner or later the day or reckoning will come, and your stock is heading back to $25. I don't know when, but do know it will happen. In the end, fundmentals triumph. You will lose and I will gain.. at your expense.

Sunday, January 09, 2005

I ran my stock screener this weekend

I ran my stock screener this weekend. Still not a lot out there worth buying. However, I did find 3 names I like. Since all of them are thinly traded, I will post my findings when (and if) my buy orders get filled.

Stockmarket returns over the next 10 years

I continue to be amazed that Wall Street analysts keep saying that they have "trimmed" their expectations for stock market returns for this year and beyond to something around 7 to 8 percent. Well, I have news for them: 7 to 8 percent, while lower than the historic average, is still way too high. Here's why. First of all, let's ask what a sensible rate of return on equities ought to be. Well, here are the facts:

1. A stock's total return is the sum of its dividend yield and its capital gain. If the market's P/E ratio is assumed to stay constant, then the capital gain (the growth in P) is equivlant to the growth in E (earnings per share).

2. The dividend yield is a function of the payout ratio (the fraction of a firm's earnings that is paid out in dividends). Historically, this has averaged about 50 percent, although this number has declined somewhat over the past 2 decades. A reasonable estimate for the dividend yield on stocks for the next 10 years is 2 percent, which is slightly more than the current dividend yield on the S&P.

3. What about capital gains? As mentioned, capital gains are a function of growth in earnings per share (EPS). Corporate profits have tended to average about 10 percent of GDP over the past century. There have been troughs (such as the Great Depression) and peaks. When was the last peak? Well, we're living in it now. Corporate earnings as a percentage of GDP are close to their historic highs. One of the reasons that corporate profits have accelerated is that productivity growth has picked up significantly since the mid-1990's. This has allowed firms to shed excess labor, which has kept wages fairly stagnant. The result: profits have jumped. In the best case scenario, real GDP growth wil contine to be strong, perhaps even rising to 4 percent over the next decade.

5. What does this imply for growth in earnings per share? Well, clearly EPS will not grow as quickly as GDP since new firms will enter the market and hence, aggregate U.S. earnings will end up being split among more firms. Also, existing firms will continue to issue new shares, thereby partly diluting existing shareholders. Historically, these two factors have implied that EPS growth has been about 2 percent lower than GDP growth. However, if corporate profits as a percent of GDP decline over the next 10 years towards their historic averge, EPS growth will lag GDP growth by more than 2 percent.

6. The market P/E is about 20 right now. The historic average is 16. Thus, if valuations decline to their historic average, the P in the P/E will grow less quickly than the E.

7. Now let's put it all together: If profits as a share of GDP stay the same and valuations do not fall, this implies that real EPS growth will be 2 percent (4 percent real GDP growth minus the 2 percent wedge between EPS and aggregate profit growth). This yields a total real return of 4 percent (2 percent dividend yield plus 2 percent capital gains). So in the case scenario, stock prices will grow by 4 percent in real terms over the next 10 years. Assuming inflation stays at around 2 percent, that's 6 percent nominal growth in stock prices. Again, this is the best case scenario. What's a "realistic scenario"? Well, a realistic scenario is one in which the market's P/E ratio declines to its historic average of 16 and corporate profits as a percent of GDP decline by about 2 percent. Taken together, this lowers expected stock returns by 4 percent per year to about 2 percent per year. And that, of course, still implies that the economy will growth at an above average pace, which is far from certain.

The bottom line is that Wall Street's "conservative" estimate of 7 to 8 percent growth in stock prices is not nearly conservative enough. In the current market environment, 2 percent is about the best bet that one can make. As Warren Buffet once said, if stock returns came from history books, librarians would all be millionaires. The fact of the matter is that historic returns have been colored by the fact that analysts have confused apples with oranges. In the late nineteenth centruy, the market's P/E was less about 5 because stocks were perceived then to be very risky, reflecting much worse corporate governance, high transaction costs, and fewer ways to diversify one's portfolio. Furthermore, the 1970's and early 80's witnessed very high inflation, which artificially boosted nominal equity returns (but not real equtiy returns). This accounts for why historically, stock market returns have averaged about 8 percent. However, future returns are likely to be a lot lower.

1. A stock's total return is the sum of its dividend yield and its capital gain. If the market's P/E ratio is assumed to stay constant, then the capital gain (the growth in P) is equivlant to the growth in E (earnings per share).

2. The dividend yield is a function of the payout ratio (the fraction of a firm's earnings that is paid out in dividends). Historically, this has averaged about 50 percent, although this number has declined somewhat over the past 2 decades. A reasonable estimate for the dividend yield on stocks for the next 10 years is 2 percent, which is slightly more than the current dividend yield on the S&P.

3. What about capital gains? As mentioned, capital gains are a function of growth in earnings per share (EPS). Corporate profits have tended to average about 10 percent of GDP over the past century. There have been troughs (such as the Great Depression) and peaks. When was the last peak? Well, we're living in it now. Corporate earnings as a percentage of GDP are close to their historic highs. One of the reasons that corporate profits have accelerated is that productivity growth has picked up significantly since the mid-1990's. This has allowed firms to shed excess labor, which has kept wages fairly stagnant. The result: profits have jumped. In the best case scenario, real GDP growth wil contine to be strong, perhaps even rising to 4 percent over the next decade.

5. What does this imply for growth in earnings per share? Well, clearly EPS will not grow as quickly as GDP since new firms will enter the market and hence, aggregate U.S. earnings will end up being split among more firms. Also, existing firms will continue to issue new shares, thereby partly diluting existing shareholders. Historically, these two factors have implied that EPS growth has been about 2 percent lower than GDP growth. However, if corporate profits as a percent of GDP decline over the next 10 years towards their historic averge, EPS growth will lag GDP growth by more than 2 percent.

6. The market P/E is about 20 right now. The historic average is 16. Thus, if valuations decline to their historic average, the P in the P/E will grow less quickly than the E.

7. Now let's put it all together: If profits as a share of GDP stay the same and valuations do not fall, this implies that real EPS growth will be 2 percent (4 percent real GDP growth minus the 2 percent wedge between EPS and aggregate profit growth). This yields a total real return of 4 percent (2 percent dividend yield plus 2 percent capital gains). So in the case scenario, stock prices will grow by 4 percent in real terms over the next 10 years. Assuming inflation stays at around 2 percent, that's 6 percent nominal growth in stock prices. Again, this is the best case scenario. What's a "realistic scenario"? Well, a realistic scenario is one in which the market's P/E ratio declines to its historic average of 16 and corporate profits as a percent of GDP decline by about 2 percent. Taken together, this lowers expected stock returns by 4 percent per year to about 2 percent per year. And that, of course, still implies that the economy will growth at an above average pace, which is far from certain.

The bottom line is that Wall Street's "conservative" estimate of 7 to 8 percent growth in stock prices is not nearly conservative enough. In the current market environment, 2 percent is about the best bet that one can make. As Warren Buffet once said, if stock returns came from history books, librarians would all be millionaires. The fact of the matter is that historic returns have been colored by the fact that analysts have confused apples with oranges. In the late nineteenth centruy, the market's P/E was less about 5 because stocks were perceived then to be very risky, reflecting much worse corporate governance, high transaction costs, and fewer ways to diversify one's portfolio. Furthermore, the 1970's and early 80's witnessed very high inflation, which artificially boosted nominal equity returns (but not real equtiy returns). This accounts for why historically, stock market returns have averaged about 8 percent. However, future returns are likely to be a lot lower.

Friday, January 07, 2005

Weekly Summary

I started nicely in the black today, but as the day wore on, my portfolio drifted down, ending down $1,000 for day. For the week as a whole however, I came out $971 ahead. Not exactly breathtaking, but considering the dreadful performance of the major indices over the past 5 trading days, I am happy with the result. Thanks to the several people who emailed me their stock suggestions. I appreciate your views. Many of your stocks look interesting and appealing, but none quite fit my investment profile. I'll run my stockscreener again this weekend, and see if anything pops up. Over the past few months, I've gotten mainly blanks, which is indeed a ominous sign, as it suggests that there aren't too many attractively priced stocks left out there, especially in the small cap universe. I would particularly appreciate your thoughts on good short candidates, as I'm trying to beef up that portion of my portfolio. Please email me your views, or leave a comment.

Thursday, January 06, 2005

AEHR's mysterious ways

Back in black today: up $7,000. AEHR reported earnings after the close, as well as announcing a new order from Sanmina. In my experience, when a company releases two press releases simultaneously, that usually means one is bad and the other is good (with the hope that the good news deflects the bad). And sure enough, the earnings were mediocre at best (eps in line, but revenues projected to decline next quarter). Initially, the stock fell 5 percent in afterhours, and then began to rally, rising 30 percent. I'm not sure why it rallied, because the conference call wasn't too enlightening as far as I could discern. Well, I sold half my shares at $4.35 (the strategy of "sell first, ask questions later" has worked well enough for me in the past, so I see no reason to deviate from it now). Tomorrow will tell whether this was a good move.

Wednesday, January 05, 2005

Investor's Buiness Daily: the tabloid of financial journalism

Investor's Business Daily proves again why it's the tabloid of financial journalism (minus the page 3 spread of Maria Bartiromo). This time it's a bizarrely inaccurate diatribe about why Social Security should be privatized:

So let me see if I got this right? The general budget of the U.S. federal government is running $400 billion plus cash deficits, but Dick Cheney isn't concerned because "As Reagan proved, deficits don't matter". The reason they don't matter is because the U.S. government can just keep issuing treasury securities to finance budget deficits. Now it is true that according to the latest estimates, by 2018 cash payments to Social Security recipients will exceed receipts from payroll taxes and the fund will have to draw on a huge stash of treasury securities that it has accumulated over the preceding years. But you see: all those IOU's in the form of treasury securities that the social security trust fund has built up aren't really worth anything. Huh? Well, let's tell that to the Chinese and Japanese central banks that have been buying them. I wonder what would happen to interest rates if they believe the editors of Investor's Business Daily? But I guess I shouldn't complain too much. Without their stupid stock recommendations, I would never have been able to short Travelzoo at $101.

The system is headed for a collision with the hard wall of reality in just 14 years. That's when Social Security's revenues will no longer cover its costs. The many who insist there is no crisis ignore reality. By every realistic actuarial estimate, Social Security is headed for a bust.

So let me see if I got this right? The general budget of the U.S. federal government is running $400 billion plus cash deficits, but Dick Cheney isn't concerned because "As Reagan proved, deficits don't matter". The reason they don't matter is because the U.S. government can just keep issuing treasury securities to finance budget deficits. Now it is true that according to the latest estimates, by 2018 cash payments to Social Security recipients will exceed receipts from payroll taxes and the fund will have to draw on a huge stash of treasury securities that it has accumulated over the preceding years. But you see: all those IOU's in the form of treasury securities that the social security trust fund has built up aren't really worth anything. Huh? Well, let's tell that to the Chinese and Japanese central banks that have been buying them. I wonder what would happen to interest rates if they believe the editors of Investor's Business Daily? But I guess I shouldn't complain too much. Without their stupid stock recommendations, I would never have been able to short Travelzoo at $101.

Down again

Smallcaps were hit particularly hard today, with the Russell 2000 down 1.76 percent, while the DOW was off only 0.3 percent. My portfolio, which is about as microcap focused as it gets, wasn't spared: down $3,100 today.

Tuesday, January 04, 2005

Another slap in the face for the little guy

Looks like the SEC plans to further tighten the rules relating to short-selling, particularly with regards to naked shorting. Disgusting! Naked shorting should be encouraged. Small companies with no analyst following are particularly vulnerable to pump and dump scams. It's also very difficult to short many of these companies since their stock is often hard to borrow. Naked shorting thus provides a strong incentive for intelligent investors to profit from the hype and hyperbole of corporate crooks and pump and dump artists by researching companies that analysts overlook and exposing any lies and distortions that they discover. This makes capital markets more efficient, and in the end, protects the small investor. The SEC should be ashamed.

My 7 day winning streak comes to a screeching end

Unlike yesterday, my portfolio was unable to avoid the NASDAQ's decent into hell, and was dragged down along with the rest of the market, down by $3,600. No major losses: just a lot of red across the board. So far, my fear that 2005 would be a down year is right on the mark. I hope (though doubt) that I'm wrong.

![]()

{kind=link}